“Financial planning guide for young doctors: Loan repayment, savings, insurance, investing, taxes, retirement, and practical steps using Dr. Joshi’s case study.”

🌟 Smart Money Moves for Young Doctors: A Complete Financial Planning Guide (Case Study: Dr. Joshi, 27)

Starting your career as a doctor is exciting — a new job, a stable income, and the freedom to make your own financial decisions. But this new phase also comes with responsibilities: repaying loans, building savings, protecting your health, and planning for a secure future.

In this guide, we break down a simple, practical, beginner-friendly financial roadmap for young doctors using the real-life profile of Dr. Joshi (27), a bachelor working in a government hospital. Everything is explained in plain language as if you’re discussing money with a close friend. Let’s get started

🧭: Understanding Dr. Joshi’s Profile (The Case Study)

Dr. Joshi is a 27-year-old doctor who has just secured a government job after completing his medical studies. His background is typical of many young doctors:

- Has an education loan

- Limited financial responsibilities

- Stable, but not very high government salary

- Wants to become financially independent

- No major goals like marriage or home purchase yet

This is the perfect stage to build strong money habits that will benefit him for life.

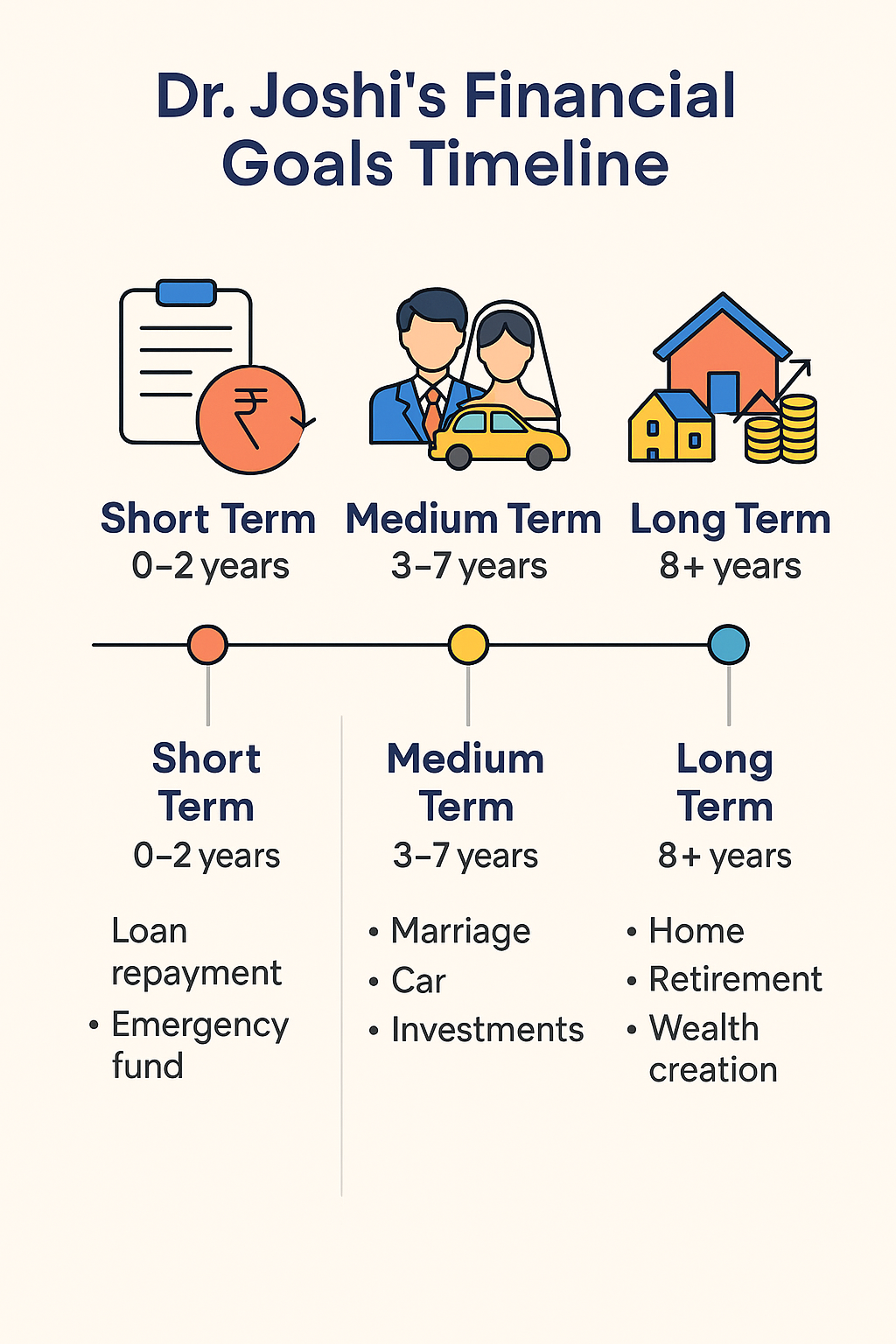

🎯 : Financial Goals for Young Doctor

Even though Dr. Joshi has no dependants or major commitments, he should define the following goals clearly:

1. Short-term Goals

- Repay education loan

- Build emergency fund

- Start health & personal accident insurance

- Control unnecessary expenses

2. Medium-term Goals

- Plan for marriage

- Save for car purchase

- Build an investment portfolio

3. Long-term Goals

- Retirement planning

- Buying a residential property

- Wealth creation

- Financial independence

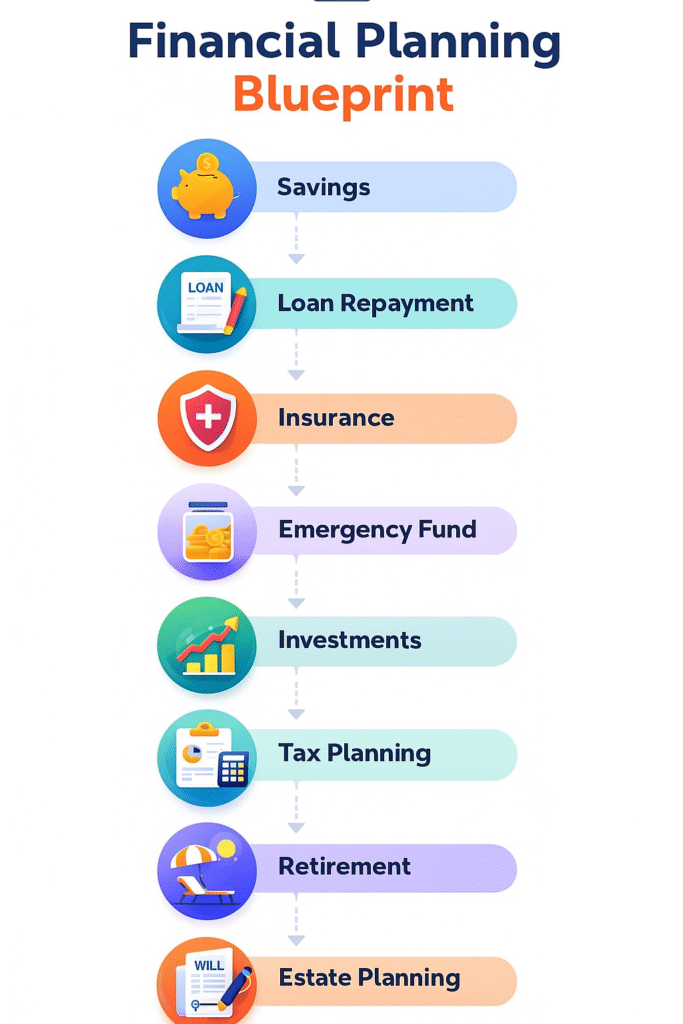

💡: Savings Strategy — The Foundation of Financial Discipline

Government salaries are stable, but not necessarily high. Many young doctors fall into the trap of lifestyle inflation. Dr. Joshi must first adopt a savings-first mindset.

The 50-30-20 Rule (Beginner Friendly Blueprint)

- 50% – Needs (rent, food, travel, utilities)

- 30% – Wants (shopping, eating out, gadgets)

- 20% – Savings & Investments

If his income is ₹60,000/month, he should save at least ₹12,000/month.

✨ Benefits of Early Saving

- Builds financial discipline

- Helps repay loans faster

- Reduces stress during emergencies

- Offers money for future goals

- Allows early investing → more compounding

- Avoids lifestyle debt

📘 : Loan Repayment Plan — Becoming Debt Free Early

Since education loans often carry 8–10% interest, clearing them quickly offers guaranteed returns.

Why Loan Repayment Must Be the #1 Priority

- Avoids interest accumulation

- Boosts credit score

- Makes future loans (car/home) cheaper

- Gives mental peace

- Frees monthly cash flow

Recommended Strategy

✔️ Pay EMIs regularly

✔️ Allocate extra savings toward principal repayment

✔️ Avoid delaying or defaulting — this harms your credit score

✔️ Close the loan within 2–4 years

⚠️ : Emergency Fund — Your Safety Cushion

Even though Dr. Joshi has job security, emergencies don’t warn before arriving.

Emergency Fund Definition

A financial reserve created to handle unexpected expenses like medical emergencies, urgent travel, sudden repairs, or income disruption.

How Much Should He Save?

📌 6 months of monthly expenses

If his expenses are ₹30,000/month → aim for ₹1.8 lakh.

Where to Keep Emergency Fund?

Choose safe, liquid instruments:

- High-interest savings account

- Liquid mutual funds

- Short-term bank deposits

🛡️: Insurance Planning — Protecting Income, Health & Life

Insurance is not an investment — it’s a protection tool.

🧍♂️: Life Insurance (Optional for Young Doctors)

Since Dr. Joshi is a bachelor with no dependants, life insurance is not mandatory.

But he should consider it if:

- His parents depend on him

- Bank requires loan insurance

- He wants low premiums at a young age

Prefer:

✔️ Term Insurance

✔️ Cover: 10–12 times annual income

🚑 H3: Personal Accident Insurance (Highly Recommended)

This is critical for young doctors.

Why?

Accidents can cause:

- Temporary disability

- Permanent disability

- Loss of income

- Increased medical expenses

A PA policy is very cheap and essential

🏥 : Health Insurance (Must Have)

Even for a doctor, medical emergencies are unpredictable.

Why he should buy early:

- Lower premiums

- Fewer exclusions

- Coverage independent of employer

He should also consider:

- Critical illness insurance

- Super top-up plans

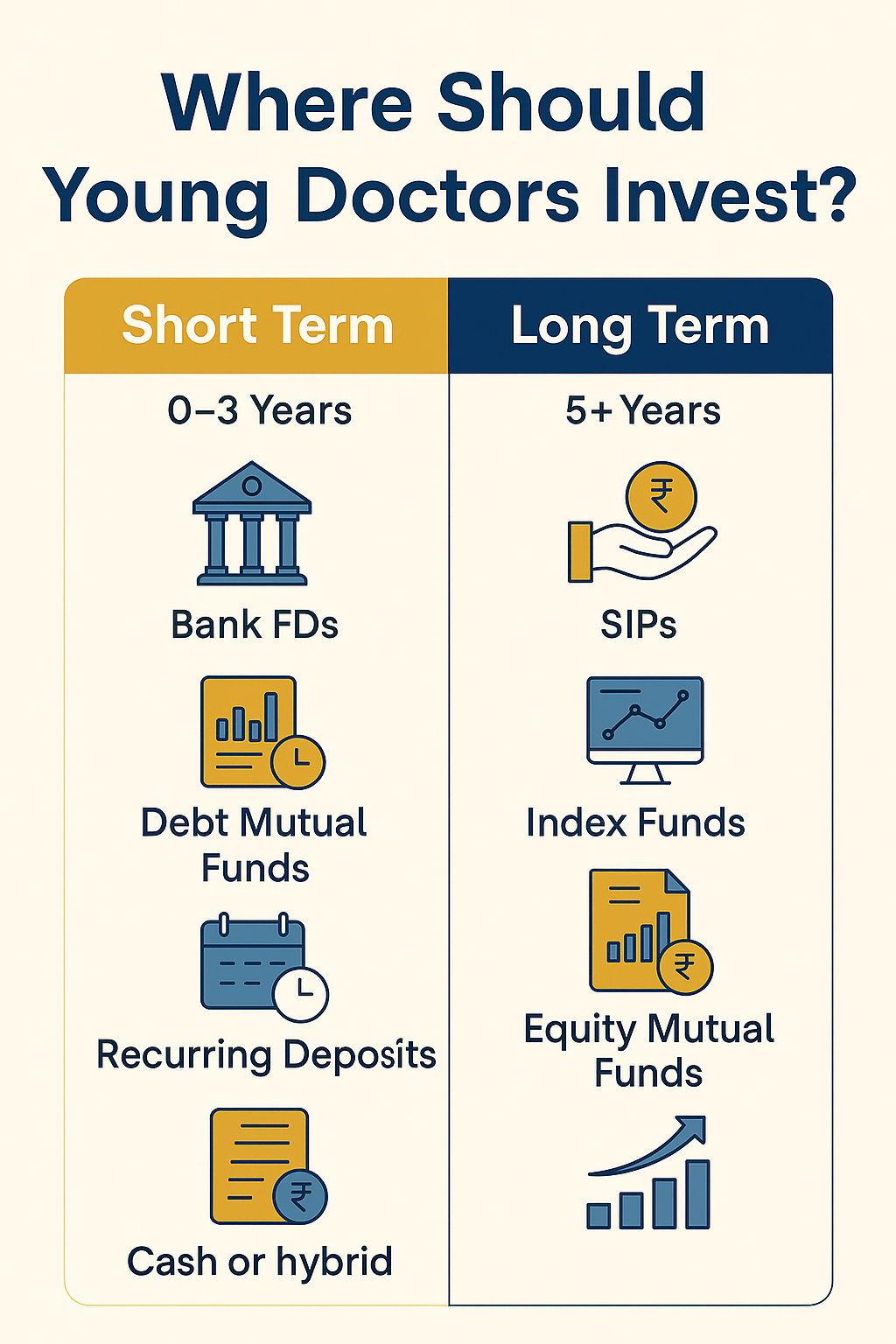

📈: Investing for Short-Term & Long-Term Goals

Once loan & insurance are sorted, Dr. Joshi should begin investing.

Short-Term Goals (0–3 Years)

Use safe, low-risk options:

- Bank FDs

- Short-term debt mutual funds

- Recurring deposits

Goals include:

- Marriage

- Gadget purchases

- Travel

Long-Term Goals (5+ Years)

Use growth-oriented options:

- Equity mutual funds

- Nifty 50 index fund

- Flexi-cap funds

- ELSS funds (also give tax benefit)

Benefits of Starting Early

- Power of compounding

- Higher returns

- Ability to take higher risk when young

- Smaller monthly contributions grow big

💸: Tax Planning for Young Doctors

Dr. Joshi should make full use of available deductions.

Section 80C – Up to ₹1,50,000

Eligible instruments:

- PPF

- ELSS

- Life insurance premiums

- NSC

- 5-year tax-saving FD

Section 80D – Health Insurance

- ₹25,000 for self

- Additional deductions for parents

Education Loan Interest

- Full deduction under Section 80E

- Available for 8 years

🏖️ : Retirement Planning — Start Early, Retire Wealthy

Starting retirement planning at 27 is a superpower.

Why Should Dr. Joshi Start Now?

Because ₹5,000 invested monthly at age 27 grows into:

- ₹1.5 crore+ by age 60 (at 12% return)

- But if he starts at 35 → Only ₹60 lakh

Compounding rewards early starters.

Best Retirement Tools

- NPS

- Equity mutual funds

- PPF

- Index funds

📜: Estate Planning — A Step Most Young Doctors Ignore

Estate planning isn’t only for older people.

Dr. Joshi should:

- Add nominees to all bank accounts

- Add nominees to insurance and MF folios

- Write a simple will once he accumulates assets

Helps his family avoid legal hassles

📋: Action Plan Summary Table

| Area | Action |

| Education Loan | Repay on top priority |

| Emergency Fund | Build 6 months buffer |

| Life Insurance | Optional |

| Health Insurance | Must have |

| Personal Accident Policy | Strongly recommended |

| Investments | Choose debt or equity based on goal |

| Tax Planning | Use all eligible exemptions |

| Retirement | Start early via SIP/NPS |

| Estate Planning | Set nominees & prepare will |

📌 Future Trends for Young Doctors (Important for Long-Term Planning)

1. Rise in Medical Inflation

Healthcare costs increasing 12–15% annually → Need more insurance.

2. Growing Opportunities Abroad

Doctors moving to UK, Australia, New Zealand require strong financial discipline.

3. Higher Awareness of Mental Health

Emergency funds & insurance help reduce financial stress.

4. Automation in Personal Finance

AI-based apps will simplify:

- Budgeting

- Investment tracking

- Health records

5. Increasing Importance of Digital Investing

Millennial doctors prefer:

- Index funds

- Robo-advisors

- App-based investments

🏁 Conclusion — Small Steps Today, Big Wealth Tomorrow

Dr. Joshi’s story represents thousands of young doctors beginning their careers. Early financial planning helps them:

✔️ Become debt-free

✔️ Build wealth

✔️ Feel financially secure

✔️ Protect their family

✔️ Live stress-free

✔️ Achieve long-term dreams

A disciplined start at 27 can create a financially confident doctor at 37, a wealthy doctor at 47, and a financially independent doctor at 57.

If you’re a young doctor reading this, remember:

Your career heals people — let your money choices heal your future.

Disclaimer: All charts, diagrams, and examples shared in this article are for educational purposes only. They are not financial advice. Investors should conduct their own research or consult a licensed advisor before investing